What is the de minimis tax rule?

Definition and basics of de minimis tax rule. Key points. Who it is useful for. How to сalculate de minimis. Examples. De minimis fringe benefits and safe harbor. De minimis tax exemption: who it is useful for.When it comes to international payments via the Internet, the de minimis tax rule states that if the amount of foreign currency that passes through a business is below certain thresholds, the business may be exempt from obligations to report the said amount to officials or pay taxes on it.

The de minimis rule usually applies in cases where the cost or administrative burden of fully complying with a tax or regulatory requirement would be disproportionate to the value or importance of the transaction.

Difference between income tax and capital gain tax

When talking about the de minimis rule in particular and taxes in general, it’s helpful to differentiate between the income tax and the capital gain tax.

A tax on income is imposed on the money earned by an individual or business during a specified period (usually a year). Income tax includes income from wages, salaries, self-employment, etc. It is taxed at various rates depending on the individual’s or business’s income level and filing status.

Capital gain tax, on the other hand, is a tax on the profit realized from the sale or exchange of certain assets (capital assets), such as stocks, bonds, real estate, or businesses. It is calculated as the difference between the current sale price and the cost or other basis of the asset and is generally taxed at lower rates than income tax, with exceptions for certain short-term gains.

How to determine what form of tax is being paid

Income tax includes income from wages, salaries, self-employment, and other sources. Capital gain tax is income gained from stocks, bonds, real estate, or businesses.

Thus, if the payment received is for goods or services provided, it is typically taxed through income tax. If the payment involves the sale of an asset (like stocks or property) and results in a profit, then it may fall under the capital gains tax category.

How to calculate de minimis

There is no universal way to determine the amount of de minimis for your company. In the US, the current de minimis threshold under Section 321 is $800. In Australia, the threshold is set at AUD $1,000; in the UK, it is £250. In the EU, a small business might not need to register for VAT on cross-border sales if their total sales to other EU countries remain below €10,000 per year.

Perks of the de minimis rule

The rule has several upsides. It reduces the administrative burden on businesses handling small cross-border payments, encourages small businesses to engage in international trade by making it less costly and complex, and prevents businesses from being taxed on small transactions that would not generate significant tax revenue.

De minimis fringe benefits

A specific case of the de minimis application is de minimis fringe benefits. This refers to the occasional benefits given by the employer and received by the employees that do not have to be reported to tax officials; these may include occasional snacks or tickets to sporting events/concerts, holiday gifts of small value (like a coffee mug).

In order to fall under the de minimis category, the benefits have to be infrequent and low in value. Since they are not eligible for taxation, they are a great way for employers to boost employee morale without significant tax implications.

Whether your business operates on a merchant model or not, it would help if you had a reliable way to collect payments from your customers. Thenumberx.com provides a simple and secure solution for setting up an online payment system on your website. You can select the payment methods you want to accept and even personalize the checkout page to match your brand. By clicking this link, you can start accepting payments on your website right away.

De minimis safe harbor

The de minimis safe harbor is a rule that exempts certain tax reporting requirements for businesses dealing with foreign currency transactions. Generally, if your total income from foreign currency transactions in a year is less than $200,000, you might be eligible for this safe harbor. Individual transactions, however, must be below $10,000.

If your foreign currency transactions fall under the de minimis threshold, you can avoid filing a Foreign Bank Account Report (FBAR), a complex form used to report foreign bank accounts and financial assets. This can save you time and effort.

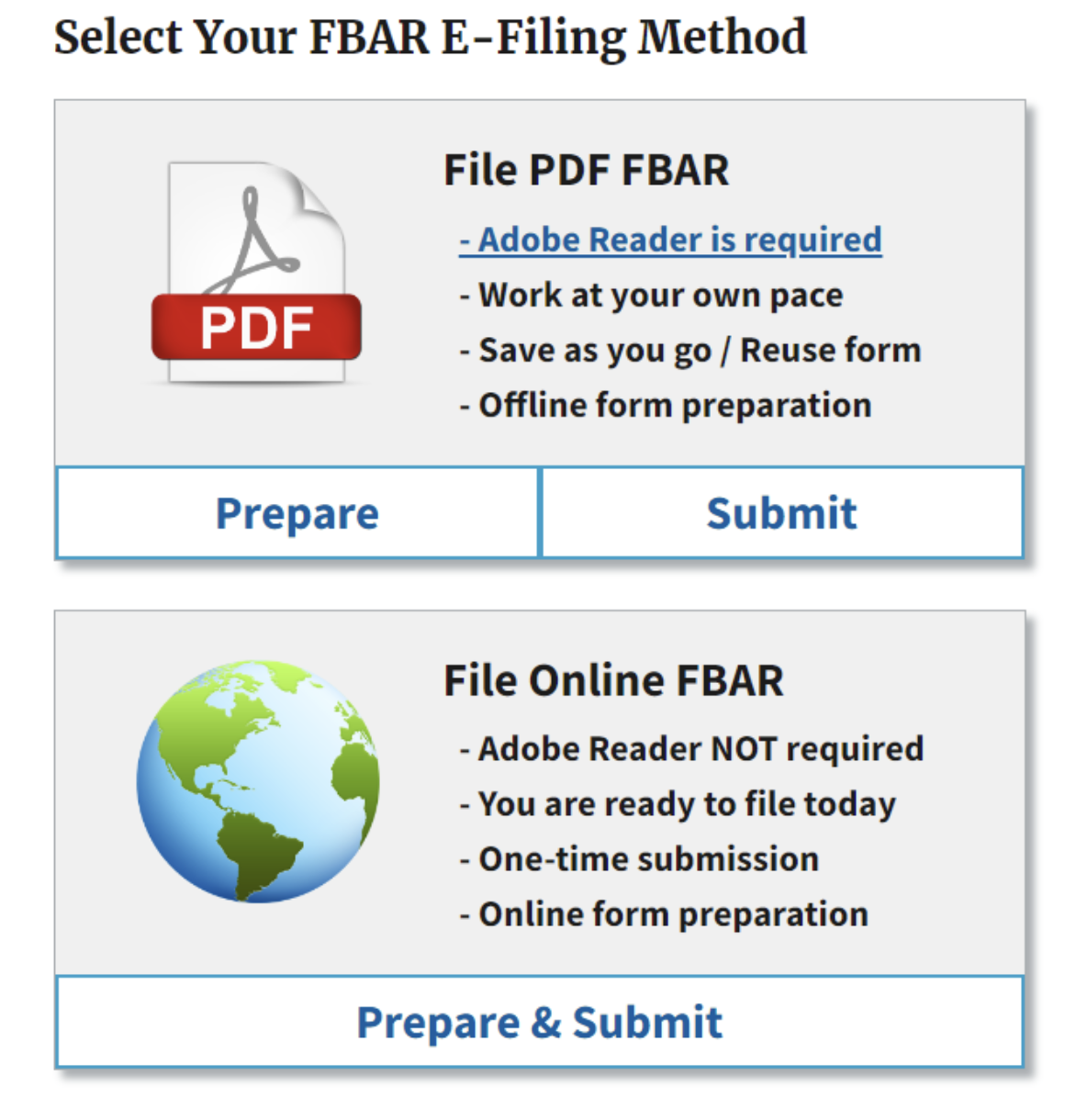

There are two methods to file FBAR: online and offline Remember that the de minimis rule is only a safe harbor, not a complete exemption. This means you might still need to report your foreign currency transactions in other ways, like on your tax return.

There are two methods to file FBAR: online and offline Remember that the de minimis rule is only a safe harbor, not a complete exemption. This means you might still need to report your foreign currency transactions in other ways, like on your tax return.How to apply for the de minimis rule

Several criteria must be met in order for a company to be eligible for the de minimis rule: the transactions must be made regularly, they must serve a legitimate business purpose, and finally, as discussed above, the value of transactions made must be below a certain value.

It is important to note that there is no universal use case for the de minimis rule: this rule may be set by statute, regulation, or administrative guidance, so before counting on it, the business employee responsible for taxing should thoroughly research the laws applicable to their particular situation.

Pay attention! Businesses should be aware of two things regarding the de minimis rule. Firstly, it may not apply to all foreign currencies. Secondly, the regulation itself may change over time in your particular jurisdiction. Thus it’s essential to consult with legal professionals before accounting for the de minimis rule being applied to you.

De minimis tax exemption

The following categories of taxpayers are exempt from paying this tax:

- Small businesses. Companies that conduct limited international sales may not exceed the threshold for taxable income, allowing them to avoid complex tax obligations.

- Freelancers and independent contractors. Individuals providing services to foreign clients can benefit from simplified reporting and reduced tax liability on smaller amounts.

- E-commerce sellers. Online retailers selling products internationally can take advantage of the de minimis exemption to minimize their tax burden on lower-value transactions.

- Digital content creators. Influencers and content creators receiving payments from abroad can avoid complicated tax filings.

- Travelers and expatriates. Individuals receiving occasional payments or gifts from abroad may find relief under the de minimis rule.

Expense vs capitalization

Expense and capitalization are another two crucial components of the taxation system.

An expense is a cost incurred by a business during an accounting period that is immediately recognized on the income statement as a reduction of revenue. Expenses are typically one-time costs that are not expected to provide future benefits; examples include salaries, rent, utilities, supplies, etc.

Capitalization is a cost incurred by a business that is not immediately recognized as an expense, but rather is recorded as an asset on the balance sheet and gradually expensed (depreciated) over its useful life. Capitalizations are costs that are expected to provide future benefits, such as equipment, buildings, and software.

Conclusion

- Getting acquainted with the de minimis rule can help you manage your financial reporting and tax obligations more efficiently.

- The de minimis tax rule specifies when the redemption of a municipal bond is considered a capital gain instead of ordinary income.

- The threshold for this classification is set at one-quarter point per full year between the time of acquisition and maturity.

- Generally, the de minimis tax rule is applicable primarily in a rising interest rate environment.

- If this rule applies to your business, you can enjoy reduced reporting and lower compliance costs.

- Merchant of record (MoR): definition8 min read / July 23, 2026

- Merchant of Record vs Payment Facilitator: What Is the Difference6 min read / July 23, 2026

- Merchant of Record vs Seller of Record: What is the difference7 min read / July 23, 2026

- What Is the Merchant Business Model?5 min read / July 23, 2026